Money habits vary from generation to generation. Boomers were known for their financial discipline and long-term planning, but millennials are often criticized for making costly money mistakes. Younger generations have different financial priorities, but some of these mistakes could have long-term consequences.

Here are some financial mistakes millennials are making that boomers would never do.

Ignoring Retirement Savings Early On

Many young adults are so focused on paying off student loans or enjoying the present that they neglect their financial future. They put off saving for retirement, thinking they have plenty of time. Their parents, on the other hand, prioritized their 401(k)s and pensions early in their careers.

The power of compound interest means that starting even a decade later can significantly reduce the amount saved for retirement.

Relying Too Much on Credit Cards

Boomers were more cautious with credit, often only using it when necessary. Millennials, however, tend to rely heavily on credit cards, sometimes racking up high-interest debt on everyday expenses. Instead of saving up for large purchases, many younger people swipe their cards without considering how much they’ll actually pay in interest.

Not Building an Emergency Fund

An emergency fund was a priority for the post-war generation, who understood that life’s unexpected expenses could derail financial stability. Young people, however, often neglect this safety net, relying on credit cards or personal loans when an emergency arises.

Without savings to cover car repairs, medical bills, or job loss, they can find themselves stuck in a financial crisis that could have been avoided with better planning.

Overspending on Rent

The baby boom generation were more likely to buy homes early in life, keeping their monthly expenses lower in the long run. Young people today, on the other hand, often choose to rent in expensive cities where housing costs take up a huge chunk of their income. With skyrocketing rental prices and stagnant wages, many are spending far more than the recommended 30% of their income on rent, leaving little room for savings.

Delaying Homeownership for Too Long

Unlike their parents, who saw homeownership as a financial milestone, many millennials are delaying or avoiding buying homes altogether. While some of this is due to high housing costs and economic challenges, many simply don’t prioritize investing in real estate.

They miss out on the benefits of building home equity and stabilizing their long-term housing costs.

Not Taking Advantage of Employer 401(k) Matching

Prudent boomers rarely left free money on the table. If their employer offered a 401(k) match, they made sure to contribute enough to take full advantage. The younger generation, however, often opt out of workplace retirement plans or contribute too little. By not maximizing employer matching contributions, they’re missing out on thousands of dollars in free retirement savings that could significantly grow over time.

Constantly Upgrading Gadgets and Technology

The older generation are cautious about technology and unlike their children don’t feel the need to buy the latest smartphone, smartwatch, or gaming system every year. This constant cycle of upgrading adds up, draining savings and leading to unnecessary spending on devices that provide only marginal improvements over older models.

Dining Out Too Often

Restaurants are seen as a treat rather than a daily habit for baby boomers, are more likely to cook at home, seeing. Millennials, however, often spend a significant portion of their income on takeout, delivery, and dining out. The convenience of fast food and meal delivery services makes it easy to overspend without realizing it.

Ignoring Life Insurance

The older folks always understood the importance of life insurance, making sure their families would be financially protected in case something happened to them. Many young people today, however, see life insurance as unnecessary or something to worry about later.

Unfortunately, waiting too long to get coverage means higher premiums and a greater risk of leaving loved ones in financial distress should an unexpected tragedy occur.

Spending Too Much on Subscription Services

Subscription services have exploded in popularity, and many millennials are paying for multiple streaming services, meal kits, fitness apps, and premium memberships. Their elders, who were more mindful of recurring expenses, wouldn’t waste money on services they barely use.

While $10 or $15 a month may not seem like much, having multiple subscriptions adds up quickly, draining money that could be better spent elsewhere.

Taking on Too Much Student Loan Debt

The older generation could afford college without going into massive debt, thanks to lower tuition costs and better job opportunities. Today’s young people, however, face soaring student loan balances that often take decades to pay off. Some debt is unavoidable but many take out loans for degrees that don’t lead to high-paying jobs, leaving them struggling to make payments well into their 40s or 50s.

Not Negotiating Salaries

The post-war generation was more likely to negotiate their salaries, knowing that starting pay significantly impacts long-term earnings. Today’s young people, on the other hand, often accept the first offer they receive, missing out on thousands of dollars in potential income.

Many feel uncomfortable negotiating or don’t realize they have the power to ask for more.

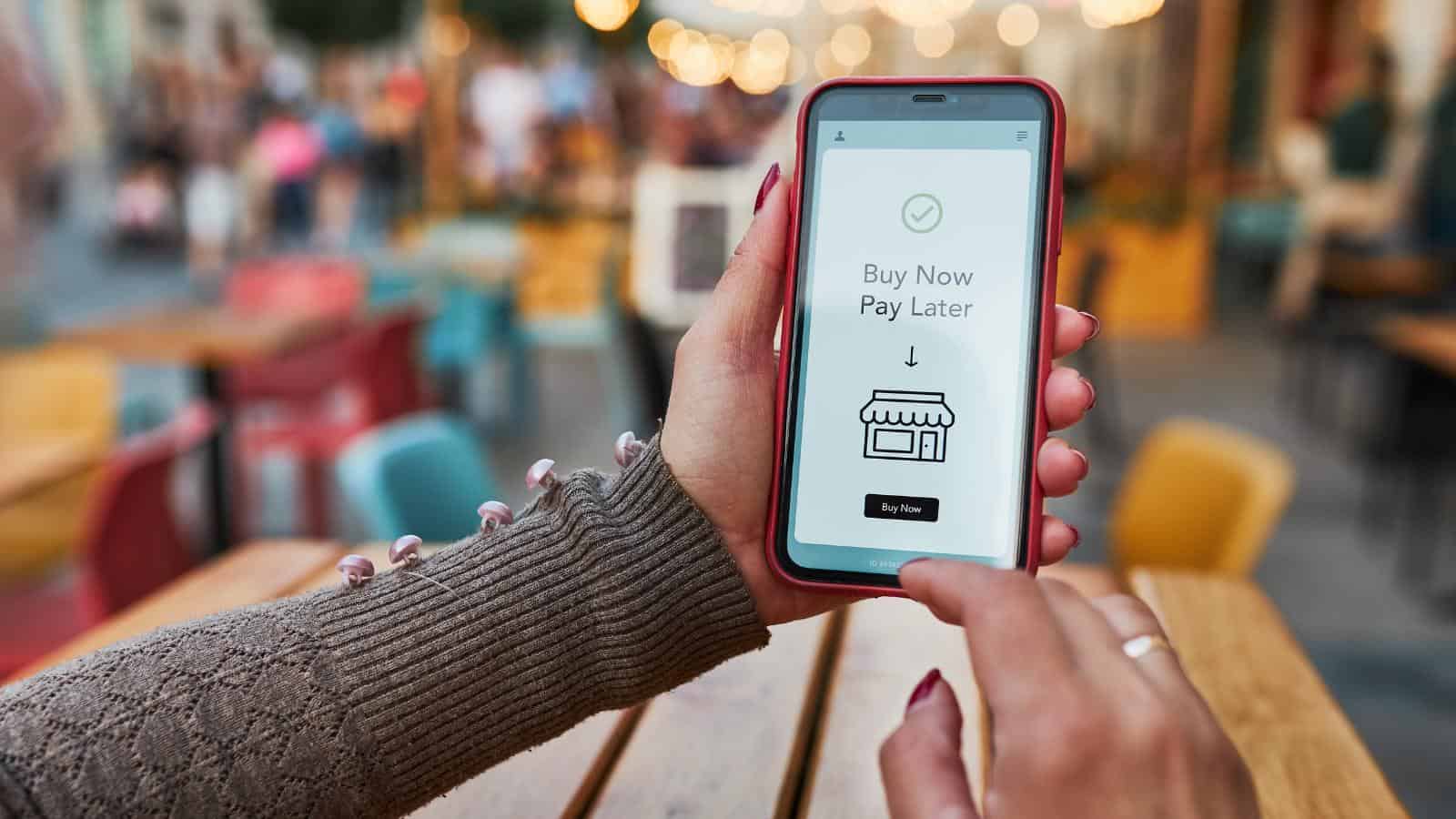

Using Buy Now, Pay Later Services

Boomers rarely bought things they couldn’t afford outright, while millennials are embracing “buy now, pay later” services for everything from clothing to electronics. These services seem convenient, but they encourage overspending and lead to unexpected debt.

When multiple installment payments pile up, it can become difficult to manage, creating financial stress that could have been avoided by budgeting properly.

Overlooking the Stock Market

Investing was a key part of the boomer generation’s wealth-building strategy, but many younger people today are hesitant to put their money in the stock market. Fear, lack of knowledge, or the belief that investing is only for the wealthy means they often leave their savings sitting in low-interest accounts.

Leasing Cars Instead of Buying

Cars were seen as long-term investments by the older generation, driving them for years to get the most value. Younger adults, however, are more likely to lease vehicles, which means they’re making perpetual car payments without ever owning anything. Leasing might seem convenient, but over time, it’s far more expensive than buying a reliable used car and driving it for as long as possible.

Depending on Side Hustles Instead of a Stable Career

Today’s young workers have embraced side hustles as a way to make extra income. This gig work can be useful, but relying too much on inconsistent earnings instead of building a stable career can be risky. Back in the day, their parents focused on long-term job security, pensions, and career growth.

Ignoring Health Insurance to Save Money

Skipping health insurance might seem like a way to save money in the short term, but it’s a dangerous gamble. The older generation prioritized having good health coverage, knowing that medical emergencies could wipe out savings.

Young people who freelance or work gig jobs, take the risk of going without insurance, only to face massive bills when unexpected medical issues arise.